Why you might want to consider lowering your lines of credit

Affiliate Disclosure: This post may contain affiliate links, which means I may earn a small commission at no additional cost to you if you make a purchase through these links. I only recommend products and services I trust and believe will benefit you. I do not sell your personal information, and all opinions expressed in this post are my own.

Editorial Disclosure: Opinions expressed here are the author's alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved, or otherwise endorsed by any of the entities included within the post..

There are certain banks that I prefer to open multiple credit cards with, and one of them is Chase Bank.

Now consider this: you open a new card and are given a huge credit limit you never plan to use. Yes, this helps your credit score increase because your credit utilization percentage just dropped.

However, even though I have multiple personal and business cards with Chase, I want even more.

These one or two accounts with larger lines of credit are now eating up all the room I have for banks to extend me even more credit for the new cards I want.

So here is what I do to “make room” to open more cards and earn more welcome bonuses. I call or secure message the bank and request they lower my lines of credit, making room for my new lines of credit and more points and miles to be earned for free vacations.

Now, you can not move credit from personal to business cards or vice versa.

Some people will say not to do this because it negatively impacts your credit utilization percentage.

To this, I say I pay my credit card statements on time and in full monthly. This makes up 65% of how everyone’s credit score is made up.

Also, I plan to open another line of credit, increasing my available credit. You see what I mean?

Here is more general information to help you understand what is truly affecting your credit score and where to put your attention.

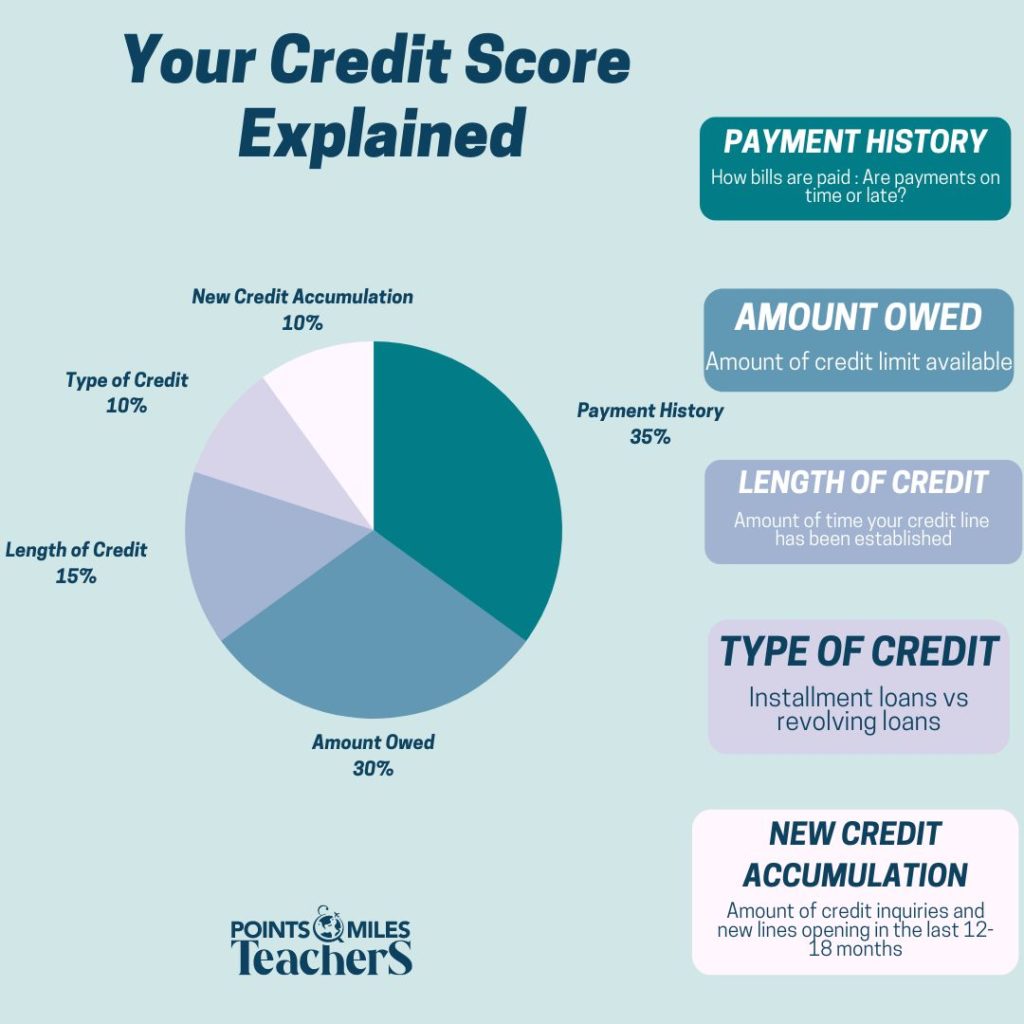

How is my credit score determined?

Your credit score is determined by several factors, including your payment history, how much debt you have, the length of your credit history, the types of credit you have, and how often you apply for new credit. Generally, the higher your score, the better your credit is considered.

Opening accounts make up 10% of your score.

Keeping the amount owed low is extremely important, along with paying off your monthly balance in full. These two combined make up 65% of your score.

Your credit history makes up 15% of your score. Keeping your oldest line(s) of credit open is essential to maintain your credit history length.

This leaves 10% of your score determined by the types of credit you hold.

How do I find out my credit score?

If you need to know your FICO credit score, you can create a free Experian account to find out and help you monitor your score.

Banks like American Express, Bank of America, Chase, Capital One, Citi, and Wells Fargo often offer these scores to their clients on their online portals.

To learn more about how credit scores are determined, check out this great article, What Is a Good Credit Score? By Louis DeNicola.

How does traveling with points and miles affect my credit score?

If you open several cards at the same time, your credit score can drop due to the increase in your credit utilization ratio. This is why I suggest pacing credit card applications 90 days apart.

I obtain many points and miles by maximizing credit card welcome bonuses and benefits to leverage them for nearly free travel.

Let’s go over how this affects credit scores.

Every 3 to 4 months, depending on welcome bonus offers or spend available categories, I consider applying for a new credit card whose points and miles align with my travel goals.

This involves a hard inquiry on my credit report. In my experience, this causes my score to drop less than 5 points before it rebounds.

Final thought

If you open cards and use them responsibly, making payments on time and, overall, opening credit cards to earn points and miles can raise your score over time.

So, if you feel like financial responsibility is your strength, traveling for nearly free with points and miles is the next natural step.

I am not a financial expert, so this is always information based on my experience.

Opinions expressed here are the author's alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

I found out about points and miles accidentally.

I was researching index funds and happened upon the points and miles community through creators who also post about budgets, financial independence, and investing.

Points and miles allowed those people to travel and work toward financial independence simultaneously.

Thank goodness I got started when I did. The past almost two years of travel have been something we will never forget.

Earning points and miles through credit cards is only a good choice if you have the financial discipline to use them, like cash/debit cards.

Since we started traveling with points and miles, we have had more money going into our investment and savings accounts than ever.

Now I'm excited to teach you!

Welcome

I am excited you are here

New to points and miles? START HERE!

")