Credit Scores & Credit Card Points: What Beginners Need to Know

Affiliate Disclosure: This post may contain affiliate links, which means I may earn a small commission at no additional cost to you if you make a purchase through these links. I only recommend products and services I trust and believe will benefit you. I do not sell your personal information, and all opinions expressed in this post are my own.

Editorial Disclosure: Opinions expressed here are the author's alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved, or otherwise endorsed by any of the entities included within the post..

If you’re just getting into the world of points and miles, you’ve probably asked yourself, “Is this going to mess up my credit score?” Great question—and I’m here to break it down in a way that’s easy to understand and stress-free to navigate.

The truth is: using credit cards to earn travel rewards can actually improve your credit score—when you use them responsibly.

Let’s walk through how your credit score works, what affects it, and how opening cards for points and miles plays into the big picture.

How Is My Credit Score Determined?

Your credit score (usually your FICO Score) is a number between 300 and 850 that lenders use to decide how “risky” it is to loan you money. The higher your score, the more trustworthy you appear—and the more likely you are to get approved for credit cards with the best rewards.

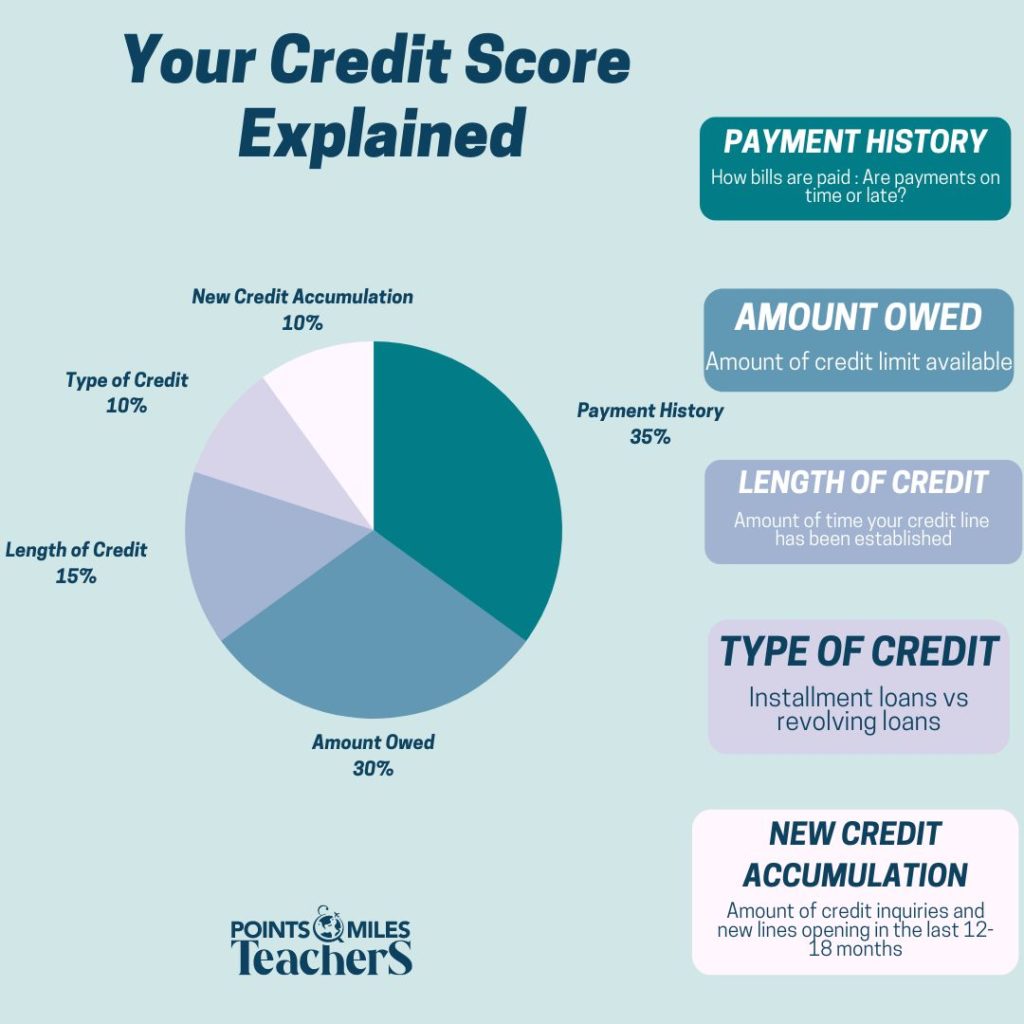

Here’s how your score is calculated:

Payment History (35%)

This is the most important factor. Always pay at least your minimum payment (preferably the full balance) on time.

Amounts Owed (30%)

This is also called your credit utilization—how much of your available credit you’re using. Try to keep this below 30%, and ideally under 10%.

Example: If you have a $10,000 credit limit and spend $3,000, your utilization is 30%.

Length of Credit History (15%)

This looks at how long your accounts have been open. Don’t close your oldest card—even if you don’t use it often. It helps your score! See more below on what to do if your oldest card has an annual fee.

New Credit / Inquiries (10%)

Every time you apply for a new card, it results in a “hard inquiry” on your credit report. This may cause a small, temporary dip (usually <5 points).

Credit Mix (10%)

This includes the types of accounts you have—like credit cards, student loans, mortgages, etc. Having different kinds of credit can help a little, but it’s not as important as payment history or utilization.

How Can I Check My Credit Score for Free?

You can check your credit score without paying a dime. Here are a few options:

Apps like Credit Karma provide VantageScores (not FICO, but still helpful for tracking trends).

Experian.com – Create a free account and monitor your FICO score.

Credit card issuers like Chase, American Express, Capital One, and Citi often show your score inside your online account.

How Do Points & Miles Affect My Credit Score?

One of the best ways to earn tons of points and miles is by opening credit cards with big welcome bonuses. But here’s the key: do it strategically.

Let’s walk through how it affects your credit:

Will opening a card hurt my score?

Yes—but only slightly and temporarily. When you apply for a new card:

- You’ll get a hard inquiry, which may drop your score by a few points.

- Your average account age may decrease.

But… you also get a bigger credit limit, which can lower your utilization (which is great!).

What to Do When Your Longest Credit Line No Longer Offers Value

If your longest line of credit is tied to a card with an annual fee that no longer offers value—especially if the rewards aren’t aligned with your current goals—it’s important to tread carefully to avoid hurting your credit score. Instead of closing the card outright, consider calling the issuer to see if you can downgrade to a no-annual-fee version. This way, you preserve your credit history and account age while avoiding the annual fee.

How often should I apply for new cards?

I recommend spacing applications about every 90 days. This gives your score time to rebound and avoids red flags from opening too many cards too fast.

My Favorite Free Tool for Tracking Credit Cards

Want help keeping track of when you opened cards, when to apply next, and how to manage bonuses?

I use and recommend Travel Freely—a free tool that helps organize your credit card strategy. No sensitive banking info required!

My Real-Life Strategy for Points & Miles

Here’s how I approach it:

Each application results in a small score dip (usually 3–5 points), but it rebounds quickly—especially since I keep my balances paid off and my utilization low.

Every 3 to 4 months, I apply for a new card that fits my travel goals and has a high welcome bonus.

I only apply when I know I can hit the minimum spend without overspending.

Final Thoughts: Can Points and Miles Improve Your Credit?

Yes—when used wisely, pursuing points and miles can actually boost your score over time.

If you:

- Pay on time

- Avoid carrying a balance

- Keep your credit usage low

- Open cards strategically

…then you’re not just earning free travel—you’re also building a solid credit profile.

Want Help Getting Started?

Drop your questions in the comments or send me a DM. I’d love to help you feel confident using credit cards the smart way—without the stress.

Opinions expressed here are the author's alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

I found out about points and miles accidentally.

I was researching index funds and happened upon the points and miles community through creators who also post about budgets, financial independence, and investing.

Points and miles allowed those people to travel and work toward financial independence simultaneously.

Thank goodness I got started when I did. The past almost two years of travel have been something we will never forget.

Earning points and miles through credit cards is only a good choice if you have the financial discipline to use them, like cash/debit cards.

Since we started traveling with points and miles, we have had more money going into our investment and savings accounts than ever.

Now I'm excited to teach you!

Welcome

I am excited you are here

New to points and miles? START HERE!

")